As the Q3 earnings season wraps, let’s dig into this quarter’s best and worst performers in the specialized consumer services industry, including ADT (NYSE: ADT) and its peers.

Some consumer discretionary companies don’t fall neatly into a category because their products or services are unique. Although their offerings may be niche, these companies have often found more efficient or technology-enabled ways of doing or selling something that has existed for a while. Technology can be a double-edged sword, though, as it may lower the barriers to entry for new competitors and allow them to do serve customers better.

The 11 specialized consumer services stocks we track reported a satisfactory Q3. As a group, revenues beat analysts’ consensus estimates by 1.1% while next quarter’s revenue guidance was 2% below.

Luckily, specialized consumer services stocks have performed well with share prices up 12.2% on average since the latest earnings results.

ADT (NYSE: ADT)

Founded in 1874 and headquartered in Boca Raton, Florida, ADT (NYSE: ADT) is a provider of security, automation, and smart home solutions, offering comprehensive services for home and business protection.

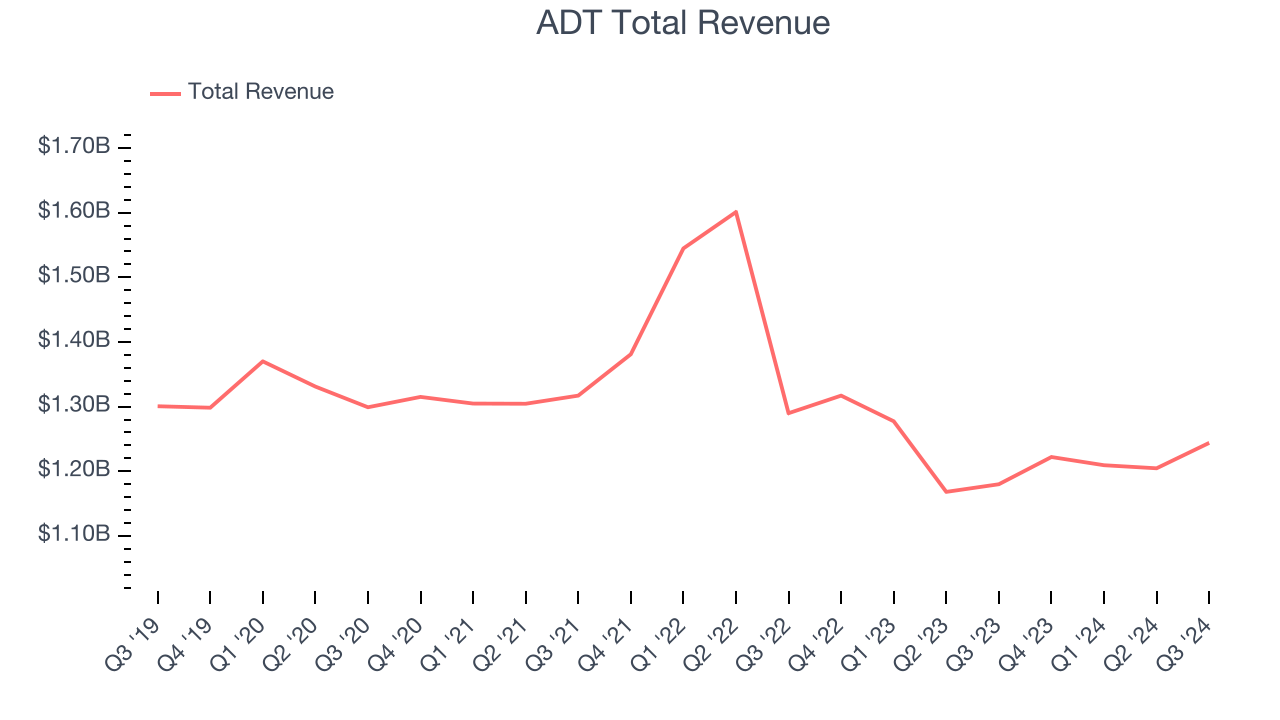

ADT reported revenues of $1.24 billion, up 5.4% year on year. This print exceeded analysts’ expectations by 1.7%. Overall, it was a strong quarter for the company with an impressive beat of analysts’ EPS estimates and full-year revenue guidance slightly topping analysts’ expectations.

“ADT delivered solid third quarter performance resulting in a record-high recurring monthly revenue balance, healthy customer retention, strong operating profitability, and cash generation. Our successful performance reflects the dedication of our employees to serve the needs of our customers,” said ADT Chairman, President and CEO, Jim DeVries.

ADT achieved the highest full-year guidance raise of the whole group. Unsurprisingly, the stock is up 7.3% since reporting and currently trades at $7.43.

Is now the time to buy ADT? Access our full analysis of the earnings results here, it’s free.

Best Q3: Matthews (NASDAQ: MATW)

Originally a death care company, Matthews International (NASDAQ: MATW) is a diversified company offering ceremonial services, brand solutions and industrial technologies.

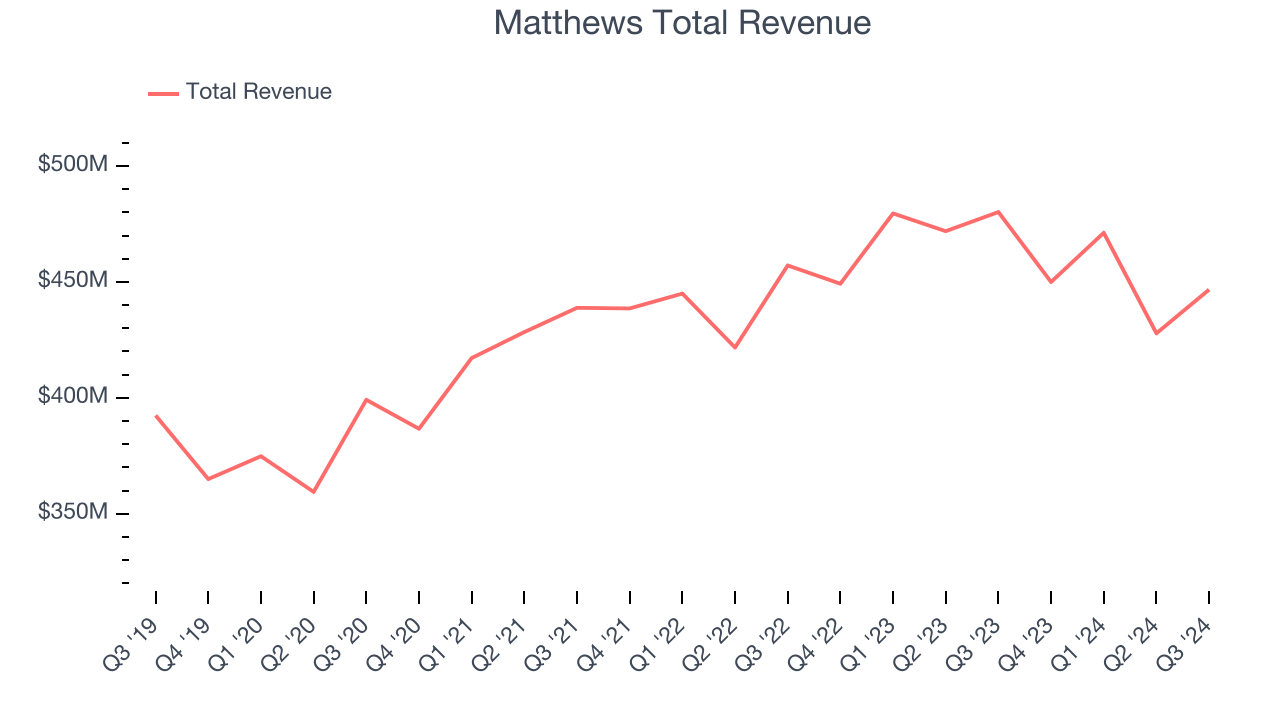

Matthews reported revenues of $446.7 million, down 7% year on year, outperforming analysts’ expectations by 1.4%. The business had an exceptional quarter with a solid beat of analysts’ EPS estimates and an impressive beat of analysts’ EBITDA estimates.

The market seems happy with the results as the stock is up 20.3% since reporting. It currently trades at $30.68.

Is now the time to buy Matthews? Access our full analysis of the earnings results here, it’s free.

Slowest Q3: 1-800-FLOWERS (NASDAQ: FLWS)

Founded in 1976, 1-800-FLOWERS (NASDAQ: FLWS) is an online retailer of flowers, gifts, and gourmet foods, serving customers globally.

1-800-FLOWERS reported revenues of $242.1 million, down 10% year on year, falling short of analysts’ expectations by 1.6%. It was a slower quarter as it posted a miss of analysts’ EBITDA estimates.

Interestingly, the stock is up 6.4% since the results and currently trades at $8.50.

Read our full analysis of 1-800-FLOWERS’s results here.

Carriage Services (NYSE: CSV)

Established in 1991, Carriage Services (NYSE: CSV) is a provider of funeral and cemetery services in the United States.

Carriage Services reported revenues of $100.7 million, up 11.3% year on year. This print topped analysts’ expectations by 8.1%. Overall, it was a very strong quarter as it also produced an impressive beat of analysts’ EPS estimates and a solid beat of analysts’ EBITDA estimates.

Carriage Services delivered the biggest analyst estimates beat and fastest revenue growth among its peers. The stock is up 22.4% since reporting and currently trades at $39.96.

Read our full, actionable report on Carriage Services here, it’s free.

Frontdoor (NASDAQ: FTDR)

Established in 2018 as a spin-off from ServiceMaster Global Holdings, Frontdoor (NASDAQ: FTDR) is a provider of home warranty and service plans.

Frontdoor reported revenues of $540 million, up 3.1% year on year. This number met analysts’ expectations. It was a very strong quarter as it also logged EBITDA guidance for next quarter exceeding analysts’ expectations and an impressive beat of analysts’ EPS estimates.

The stock is up 15.9% since reporting and currently trades at $57.35.

Read our full, actionable report on Frontdoor here, it’s free.

Market Update

In response to the Fed's rate hikes in 2022 and 2023, inflation has been gradually trending down from its post-pandemic peak, trending closer to the Fed's 2% target. Despite higher borrowing costs, the economy has avoided flashing recessionary signals. This is the much-desired soft landing that many investors hoped for. The recent rate cuts (0.5% in September and 0.25% in November 2024) have bolstered the stock market, making 2024 a strong year for equities. Donald Trump’s presidential win in November sparked additional market gains, sending indices to record highs in the days following his victory. However, debates continue over possible tariffs and corporate tax adjustments, raising questions about economic stability in 2025.

Want to invest in winners with rock-solid fundamentals? Check out our Hidden Gem Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.