Qualcomm (QCOM) posted solid earnings but a weaker-than-expected outlook. In its second quarter, EPS of $2.65 beat by nine cents. Revenue of $10.59 billion, down 3.6% year-over-year (YoY), was in line with estimates.

Unfortunately, the company’s guidance disappointed Wall Street. Management projected third-quarter revenue of $9.2 billion to $10 billion (which is below estimates of $10.18 billion) and EPS between $2.10 and $2.30 (which is below estimates of $2.43). The weakness wasn’t a big mystery, as the company continues to deal with memory-chip shortages and as China has cut inventory levels to adjust to softer market demand for smartphones.

Initially, the QCOM dipped on the news. But the negativity didn’t last long. In fact, since posting earnings on April 29, QCOM has exploded from about $152 to a recent high of $192.57 a share.

What Changed Investor Sentiment Wasn’t the Quarter—It Was What Came Next

During the company’s earnings call, CEO Cristiano Amon said Qualcomm would begin shipping data center chips to “a large hyper scaler” within the year, as noted by CNBC. While the company did not disclose which company it’s shipping chips to, it marks Qualcomm’s most serious push yet into AI infrastructure. In short, instead of focusing on a negative outlook, Wall Street shifted its focus to Qualcomm’s potential role in a booming global AI data center market—one that could be worth nearly $2 trillion by 2032, according to Markets and Markets.

Setting itself apart from companies dominating AI training in data centers, Qualcomm is putting more emphasis on running AI models efficiently, building on its strength in mobile chips. Analysts at Wells Fargo added, “QCOM is formally entering the custom silicon space following the AlphaWave acquisition, notably announcing a design win with a major hyper scaler (ship starting in Dec qtr) that it believes could be a multi-gen engagement. QCOM emphasized its DC strategy also includes merchant chips - noting development of DC CPU (focus on Agentic workloads) & inference accelerators remains on track,” as quoted by Seeking Alpha.

What Do Analysts Say About QCOM Stock?

Qualcomm’s guidance miss would have been a major selling point. But thanks to news of its future with AI data centers, Wall Street shrugged off the negativity. In addition to the AI data center news, CEO Amon also said China’s smartphone sales will bottom in the current quarter because “customers are running out of inventory,” as quoted by CNBC.

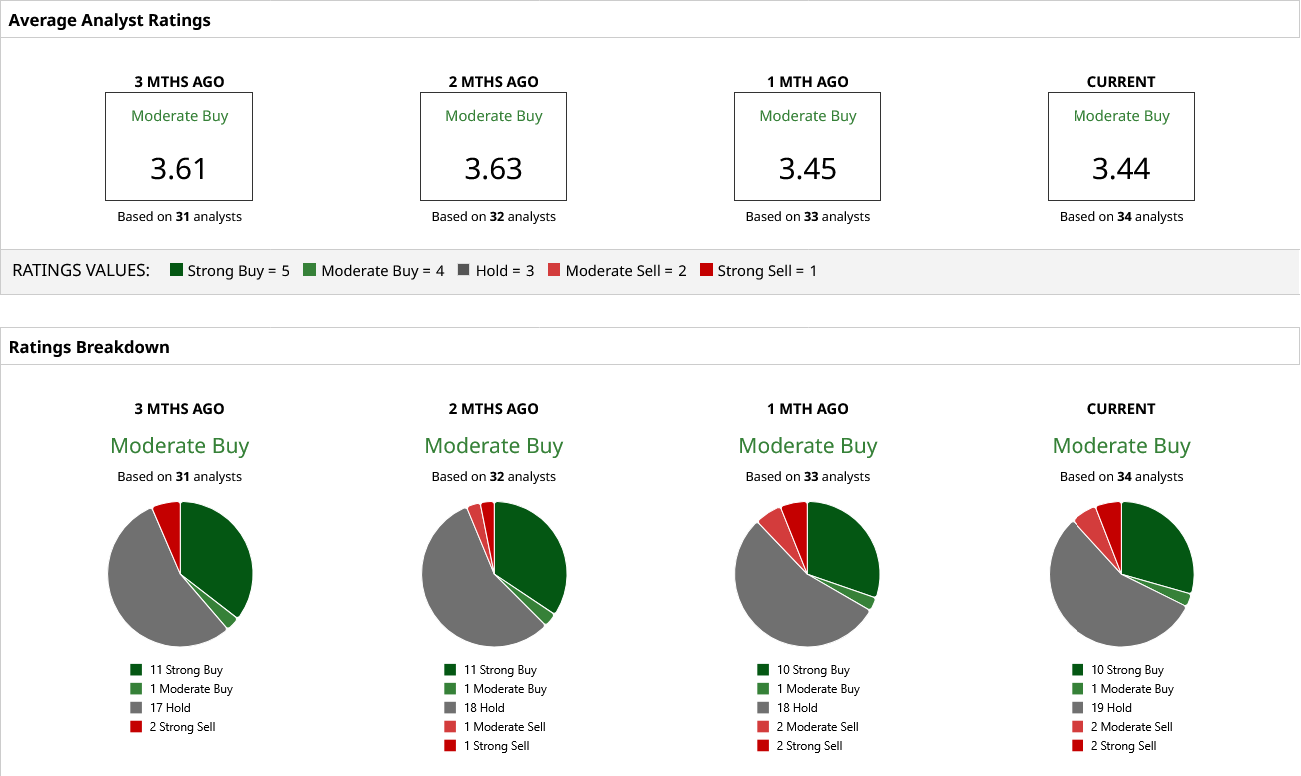

Of the 34 analysts covering the Qualcomm stock, 10 have a “Strong Buy” rating, one has a “Moderate Buy” rating, 19 have a “Hold” rating, two have a “Moderate Sell” rating, and two have a “Strong Sell” rating. The mean target price of $174.07 implies 10% potential downside from current levels. Meanwhile, the high-end target of $300 implies as much as 56% possible growth from here. While the company missed guidance and has some near-term headwinds, investors appear more focused on where Qualcomm is headed rather than where it is today. Its push into AI-driven data centers offers a strong growth catalyst.

On the date of publication, Ian Cooper did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Qualcomm Missed on Guidance. Investors Are Shrugging It Off as They Wait for Data Centers to Take QCOM Stock Higher.

- Archer Aviation Stock Soars 10% as Flying Taxi Launch Inches Closer

- McDonald’s Stock Looks Tasty Here as Investors Gobble Up Value

- SMCI Stock Is in the Doghouse. Super Micro Computer Is Hoping Nuclear Data Centers Can Help Get It Out.