Cloud giant Amazon (AMZN) will invest $5 billion in AI startup and Claude-maker Anthropic, with commitments to pump in up to $20 billion in additional capital in the coming years. Anthropic will make use of Amazon's custom chip, Tranium, as well as their ARM-based processor, Graviton, to train their AI models.

Commenting on the development, Amazon CEO Andy Jassy said, "Anthropic's commitment to run its large language models on AWS Trainium for the next decade reflects the progress we've made together on custom silicon, as we continue delivering the technology and infrastructure our customers need to build with generative AI."

After an initial pop on the news, shares of Amazon have retreated slightly. The $2.7 trillion market cap company's stock is up 8.75% on a year-to-date (YTD) basis.

Thus, the market appears to be fairly indifferent about it. But should it be, or is it ignoring Amazon's AI credentials? Let's find out.

Claude, Cloud & More: Amazon's AI Prowess Is Hard To Ignore

At the onset, I must be forthright and admit that at the current juncture, Google's (GOOGL) (GOOG) Tensor Processing Unit, or TPU, is leading the race in custom ASICs. With names like Apple (AAPL), Meta (META), and Anthropic itself onboarded as customers, Amazon's Tranium set of chips is looking up at TPU in the custom chip ladder. However, with $20 billion in annualized revenue run rate (ARR) already reached for its custom chip division, Amazon is already a serious contender.

Amazon's chip division is home to several key proprietary technologies. Trainium serves as the company's purpose-built silicon for AI training and inference workloads, while Graviton functions as a general-purpose CPU that now powers a substantial share of computing operations across AWS infrastructure. Rounding out the lineup is the Nitro System, a dedicated platform managing security protocols and networking functions.

Notably, CEO Andy Jassy has signaled that demand for these processors has reached a point where Amazon may soon begin offering rack-level configurations directly to external buyers. Jassy believes this business line carries the potential to generate an annual recurring revenue figure of $50 billion, a move that would place the company in direct competition with Nvidia (NVDA) and Advanced Micro Devices (AMD).

On the supply front, the picture looks increasingly favorable. Capacity from Trainium 2 has been completely absorbed by existing customers, and Trainium 3, which began reaching customers at the start of 2026, is already fully subscribed. Perhaps most telling is the reception for Trainium 4, a chip still approximately 18 months away from broad availability, which has already begun attracting advance orders from prospective buyers. Moreover, Trainium3, built on TSMC's 3nm process, delivers 2.52 petaflops of FP8 compute per chip with 144 GB of HBM3e memory, representing a 4.4x performance improvement over Trainium2 with 4x better energy efficiency, with customers already reporting 50% lower training and inference costs versus GPU alternatives.

Notably, where Trainium holds a structural advantage is in its tight integration within the broader AWS ecosystem and its flexibility across both training and inference workloads. Trainium's head architect has noted that the chip delivers 30% to 40% better price performance compared to other hardware vendors within AWS and that Trainium chips serve both inference and training workloads quite effectively.

Looking at the roadmap, Trainium4 is expected to begin delivering in 2027, promising 6 times the FP4 compute performance, 4 times more memory bandwidth, and 2 times more high-bandwidth memory capacity than Trainium3. Perhaps most strategically significant, a key development for Trainium4 is its planned support for Nvidia's NVLink Fusion interconnect technology, allowing AWS to build heterogeneous clusters that blend its custom silicon with Nvidia hardware rather than forcing customers to choose between ecosystems.

Moving to Claude, Amazon's investment of about $8 billion in 2023 has proved to be a masterstroke, just like Microsoft's (MSFT) was with ChatGPT. With Amazon's ownership of Anthropic expected to be between 16% and 18% currently, and the latter's valuation already hovering around $380 billion, the e-commerce giant is already sitting on some nifty profits. Moreover, with it being the primary training and cloud partner of Anthropic, Amazon is also bringing in some serious revenue from the company.

Financials in a Healthy Place (Despite Earnings Miss)

During the fourth quarter of 2025, Amazon reported net sales of $213.4 billion, representing a 14% increase compared to the same period a year earlier. The AWS segment delivered particularly strong results, posting revenue of $35.6 billion, a gain of 24% on an annual basis. Earnings per share came in at $1.95, a 4.8% improvement over the prior year's figure, extending the company's streak of year-over-year (YoY) earnings growth to nine consecutive quarters. Despite this progress, the result fell marginally short of the consensus estimate of $1.97, marking the first time in nine quarters that Amazon failed to meet bottom-line expectations.

From a cash flow perspective, net cash generated from operating activities reached $54.5 billion for the period, climbing 19.3% relative to the year before. Amazon wrapped up the full year 2025 holding a cash balance of $86.8 billion, carrying no short-term debt obligations on its balance sheet.

Looking ahead, management has guided for first quarter 2026 revenues in the range of $173.5 billion to $178.5 billion. The midpoint of that range would translate to an annual growth rate of approximately 13%.

On the valuation front, the picture presents a degree of contrast. The AMZN stock currently trades at a premium relative to broader industry benchmarks, yet sits at a discount when measured against its own historical averages. Forward multiples for P/E, P/S, and P/CF stand at 32.09, 3.30, and 16.44, each above their respective sector medians of 16.31, 0.94, and 10.21. That said, these same metrics trail the stock's five-year historical averages of forward P/E of 162.72 and forward P/CF of 10.21 by a considerable margin.

Analyst Opinion on AMZN Stock

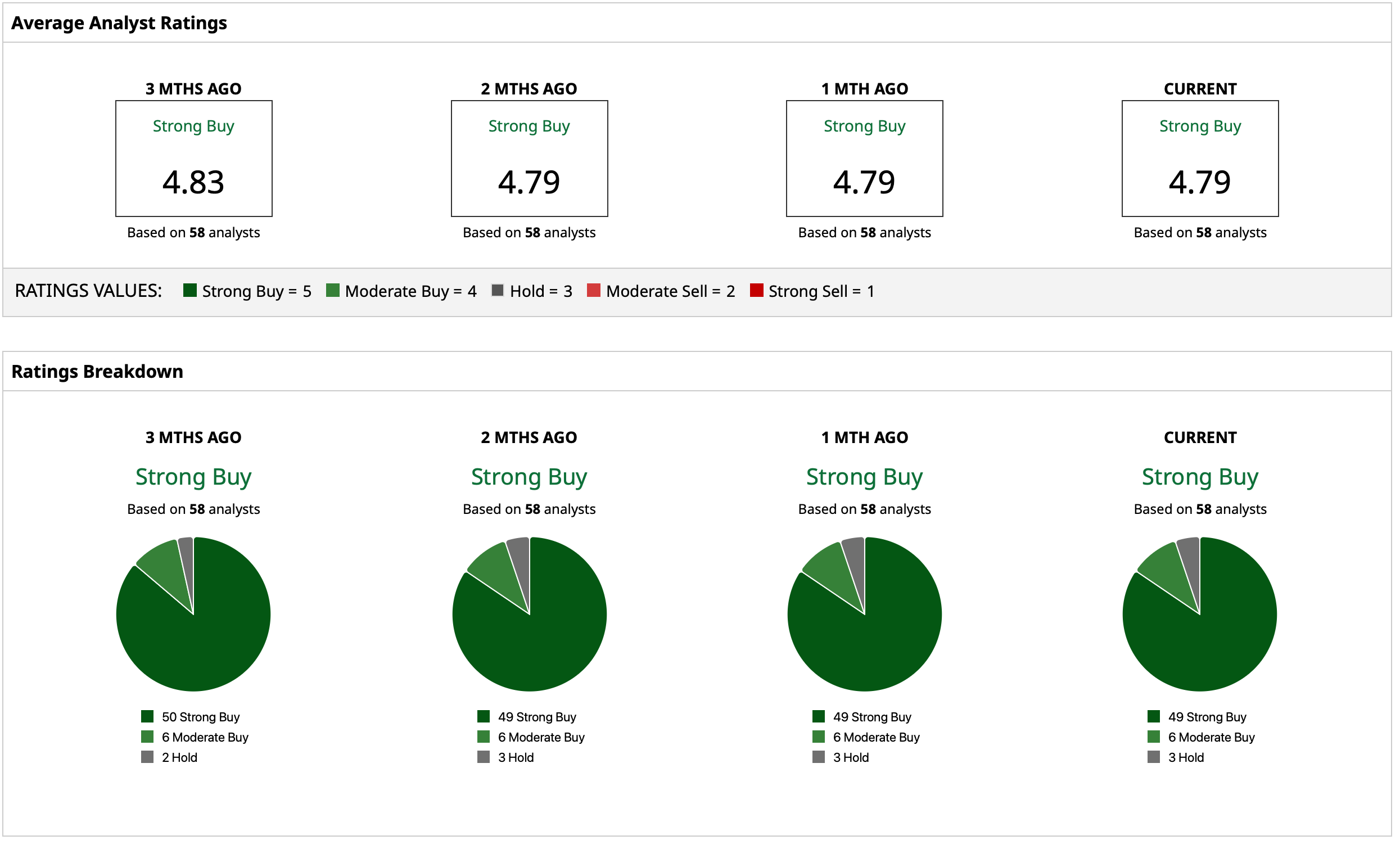

Thus, analysts remain bullish about the AMZN stock, earmarking for it an overall rating of “Strong Buy.” The mean target price of $286.66 denotes an upside potential of about 15% from current levels. Out of 58 analysts covering the stock, 49 have a “Strong Buy” rating, six have a “Moderate Buy” rating, and three have a “Hold” rating.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Axe Compute Soars on $260M Nvidia Deal. Is It Too Late to Buy AGPU Stock?

- This Delta Insider Just Slashed His Stake by More Than One-Fifth (21%). Is It Time to Follow Suit and Ditch DAL Stock?

- AMD Stock Just Hit New All-Time Highs. Should You Buy Shares Here?

- The ‘ChatGPT Moment’ for Cadence Design Systems Might Just Have Arrived, Says Needham. Should You Buy CDNS Stock Now?