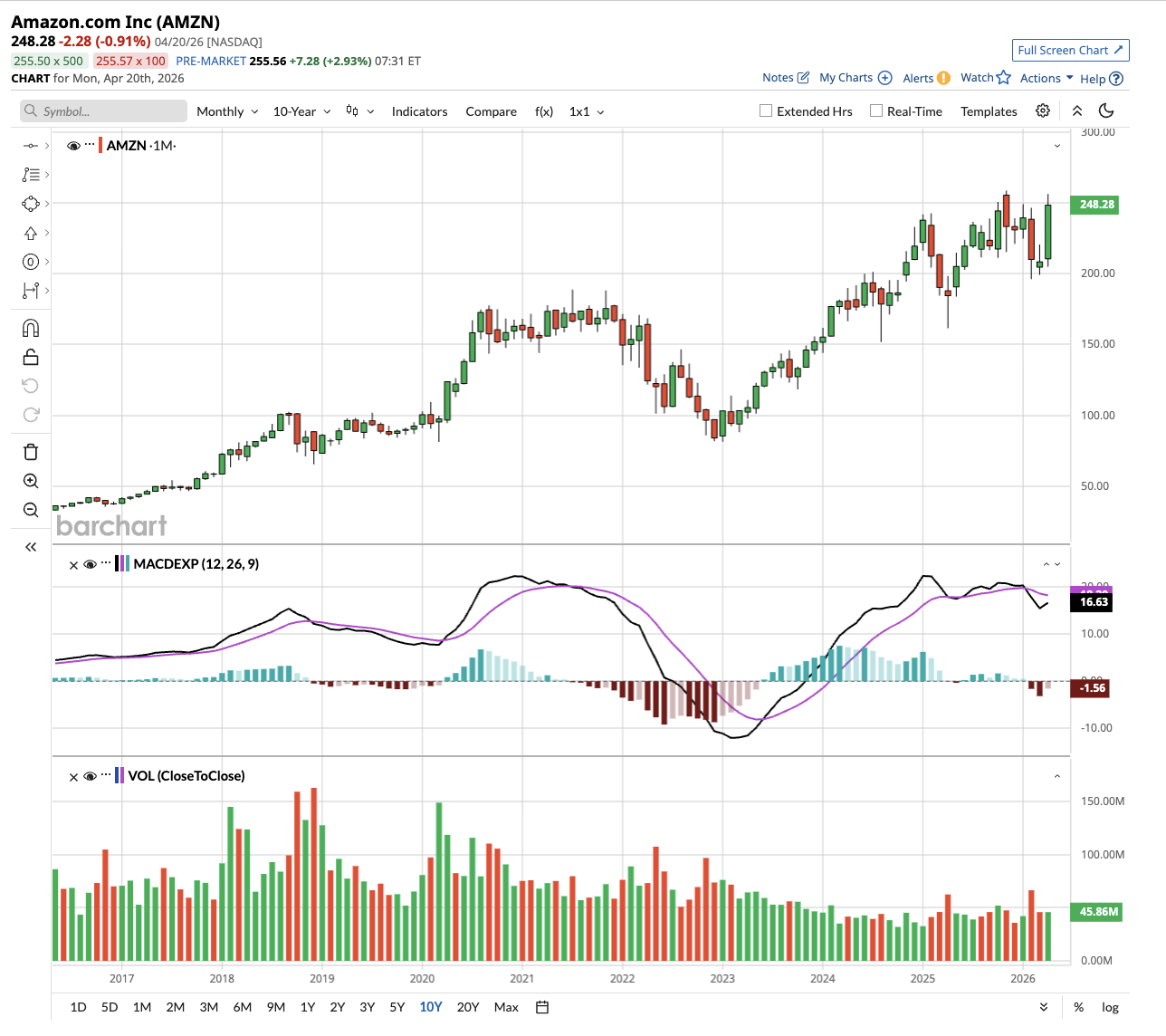

Wall Street has plenty of opinions on Amazon (AMZN). Some see massive upside, while others worry about the company's enormous spending plans. Barclays is planting its flag firmly in the bull camp — and it's backing that call with some very compelling numbers.

Barclays believes AMZN stock is positioned to outperform other mega-cap tech stocks, pointing to a wave of new disclosures from Amazon's shareholder letter. Barclays argues these disclosures make the case for Amazon Web Services (AWS) even stronger than before.

Amazon's AI Business Is a Key Driver

To understand why Barclays is bullish, it helps to know what AWS is and why it matters so much to Amazon's future. AWS is the tech giant's cloud computing division. It rents computing power, storage, and software tools to businesses of all sizes, from scrappy startups to Fortune 500 giants. It's also where Amazon is making its biggest bets on artificial intelligence (AI).

Cloud and AI are deeply connected. Companies that want to run large-scale AI workloads need massive computing infrastructure, and AWS is one of the few entities on earth with that kind of scale.

That's the backdrop for why Barclays is so excited. According to Amazon's latest disclosures, AWS AI revenue reached a $15 billion annualized run rate (ARR) in the first quarter of 2026. Barclays also believes that figure is “ascending rapidly.” For context, CEO Andy Jassy reported in February that AWS grew 24% year-over-year (YOY) in Q4 2025, its fastest growth rate in 13 quarters, making it a $142 billion ARR business.

Barclays noted that, while Amazon's AI position has long been "one of the more highly debated" topics among investors, the fresh data provides "additional confidence around AWS upside from AI over coming years."

Barclays Says the AWS Chip Business Is a $50 Billion Asset

Amazon's custom chip unit is also raking in sales at an accelerated pace. Amazon disclosed that its chips division, which includes the Trainium and Graviton processors, now runs at an annual revenue rate of $20 billion. Barclays pointed out that if the chip business were sold to outside customers as a standalone operation, it "would be ~$50 billion." That's a striking number for a business most investors barely think about.

Jassy made it clear in Amazon's Q4 earnings call that Trainium2 already powers the majority of the company's Bedrock AI service. The newer Trainium3 chip is 40% more cost-efficient than its predecessor, and Amazon expects “nearly all Trainium3 supply of chips […] to be committed by mid-2026.”

Beyond chips, Barclays flagged another data point: Amazon's plan to add more than 1 million Nvidia (NVDA) GPUs across 2026 and 2027. The bank estimates that capacity, once fully deployed, could potentially support roughly $100 billion in annual AWS revenue.

Amazon’s Grocery Moat

AWS gets most of the headlines, but Barclays also highlighted something on the retail side that's easy to overlook: Amazon's grocery segment crossed $150 billion in U.S. gross sales in 2025. That makes it the country's second-largest grocer, a fact that would have seemed absurd just a few years ago.

On the earnings call, Jassy noted that everyday essentials now account for every one in three units sold by Amazon in the United States. Customers who buy perishables from Amazon end up shopping with the company “twice as often as customers who don't.” That kind of engagement data is what investors should be paying attention to. It suggests Amazon has now become a daily habit for tens of millions of Americans.

What's Barclays' takeaway? Amazon's competitive position across cloud, AI, chips, and retail gives AMZN stock a durable edge. Barclays believes the bull thesis is well supported and that AMZN stock has the runway to keep outpacing its mega-cap peers.

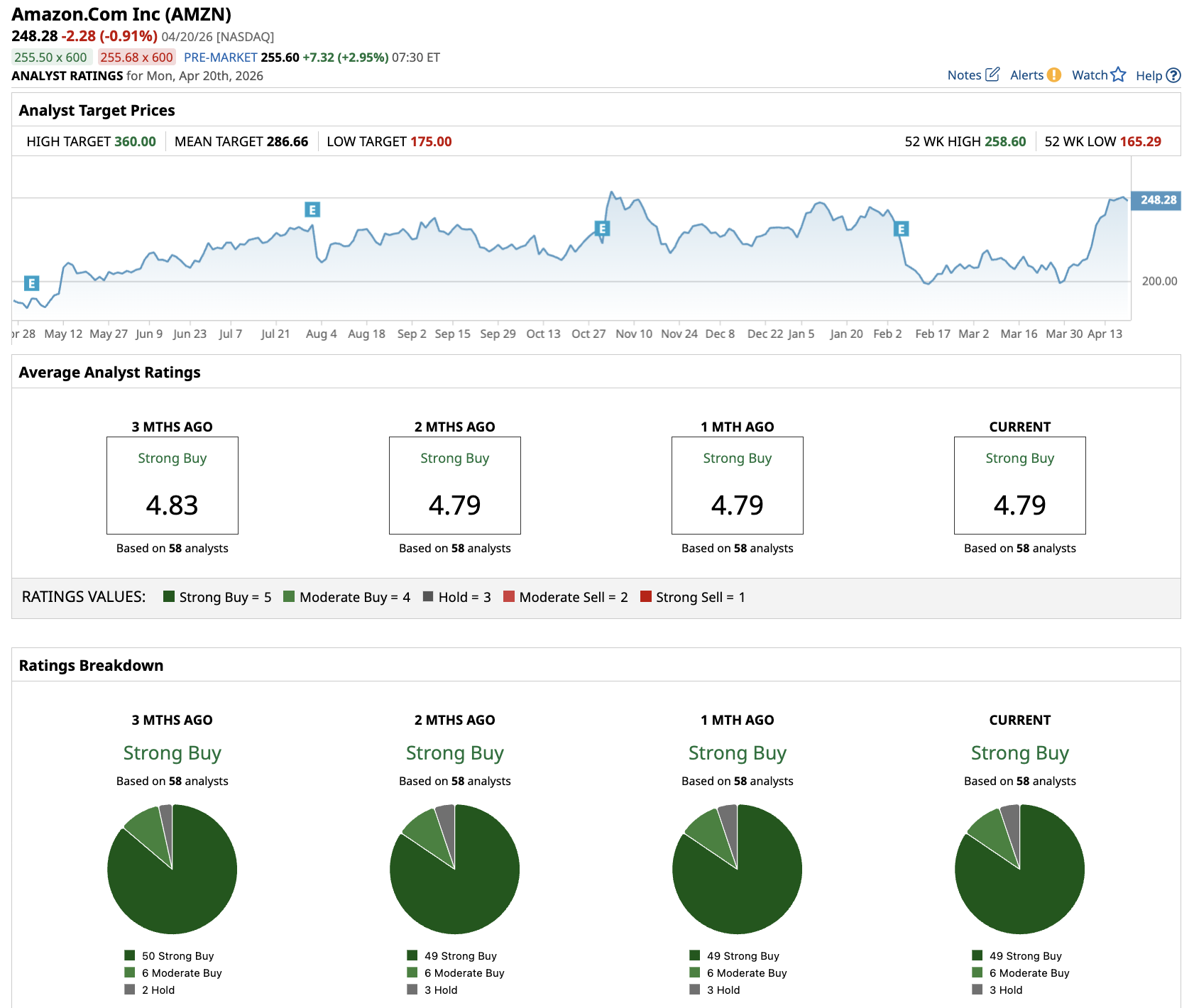

What Do Analysts Think of Amazon Stock?

Analysts tracking AMZN stock forecast adjusted EPS to expand from $7.17 per share in 2025 to $16.34 in 2030.

Overall, Amazon has a consensus “Strong Buy” rating. Out of the 58 analysts covering AMZN stock, 49 recommend a “Strong Buy,” six recommend a “Moderate Buy,” and three recommend a “Hold" rating. The average price target is $287.79, which implies 13% potetnial upside from here.

On the date of publication, Aditya Raghunath did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- This Dividend Stock Keeps Hitting It Out of the Park: Should You Buy?

- Should You Buy the Dip in United Airlines Stock?

- Axe Compute Soars on $260M Nvidia Deal. Is It Too Late to Buy AGPU Stock?

- This Delta Insider Just Slashed His Stake by More Than One-Fifth (21%). Is It Time to Follow Suit and Ditch DAL Stock?