The "Big Short" investor is doubling down on his bearish bet against Palantir Technologies (PLTR), but Wall Street isn't convinced. Michael Burry has been betting against the artificial intelligence (AI) software company since the fall of 2025.

Even after President Donald Trump publicly praised Palantir's military capabilities in a Truth Social post, Burry held firm. In a Substack post, Burry stated that he continues to hold long-dated put options on PLTR.

PLTR stock fell nearly 14% last week and is down roughly 23% in 2026. Valued at a market cap of $316 billion, PLTR stock is up more than 1,500% over the past three years. So is the ongoing drawdown a buying opportunity for long-term investors?

Wedbush Says Burry Has It Wrong on PLTR

In a post on X on April 9, Wedbush Securities analyst Dan Ives called Burry's narrative about Anthropic displacing Palantir "the wrong take and a fictional narrative," arguing that Palantir remains "at the epicenter of the AI Revolution" and is a "core AI winner."

Ives doubled down on this sentiment in a more recent analyst note, stating that Palantir “remains one of our top tech picks, and the recent fictional bear narrative by Burry and others will be proved emphatically wrong.”

Burry had argued in a post that he later deleted from X that Anthropic's rising enterprise presence signals a shift in AI spending away from companies like Palantir.

Futurum CEO Daniel Newman pushed back on Burry’s thesis, pointing out a critical fact that makes the Anthropic threat look a lot smaller: Anthropic is currently blacklisted by the Pentagon, and the U.S. government is Palantir's single largest customer.

The Pentagon wants to designate Anthropic as a national security risk, a move that was halted by the federal appeals court in Washington. Anthropic is facing significant headwinds as it competes with Palantir in the government segment.

Palantir's Q4 Numbers Were Spectacular

Palantir’s lofty valuation is supported by robust growth numbers.

- In Q4 of 2025, it grew the top line by 70% year-over-year (YoY), the highest rate as a public company.

- Its U.S. business, which accounts for 77% of total revenue, surged 93% YoY.

- U.S. commercial revenue also jumped 137%.

The company's "Rule of 40" score, a key metric that combines revenue growth and profit margin, hit 127%. For context, most high-performing software companies aim to consistently surpass the 40% threshold.

Chief Financial Officer Dave Glazer guided to full-year 2026 revenue of $7.19 billion, representing 61% YoY growth. Further, the AI-powered tech stock is expected to remain GAAP-profitable every quarter this year.

Chief Revenue Officer Ryan Taylor noted that 61 deals over $10 million were closed in the quarter alone. One healthcare company signed a $96 million deal after just two boot camps with Palantir's platform. An engineering services firm signed an $80 million deal after a series of demos, showcasing a steady rise in enterprise-wide commitments.

New Deals Show Palantir Is Expanding Its Reach

Palantir renewed and expanded a five-year deal with Stellantis (STLA). The automaker will extend its use of Palantir Foundry and begin deploying the Palantir Artificial Intelligence Platform (AIP) across select business functions.

Consulting giant Bain & Company also expanded its partnership with Palantir. The two firms have been collaborating since last year, combining Palantir's AI platforms with Bain's industry expertise to help clients accelerate data-driven decision-making and cost efficiency. Under the broader arrangement, Bain will scale AI-powered transformations for clients using Palantir's software and forward-deployed engineers.

Palantir also announced a deal with Moder, a mortgage technology company, to build an AI-powered mortgage operations platform. The first pilot customer is Freedom Mortgage. The platform is designed to streamline loan servicing and improve accuracy for homeowners.

On the defense side, ShipOS, Palantir's platform for accelerating U.S. submarine production, is gaining traction across shipbuilders and suppliers. Chief Technology Officer Shyam Sankar said one shipbuilder reduced planning time from 160 hours to 10 minutes.

Should You Buy PLTR Stock Now?

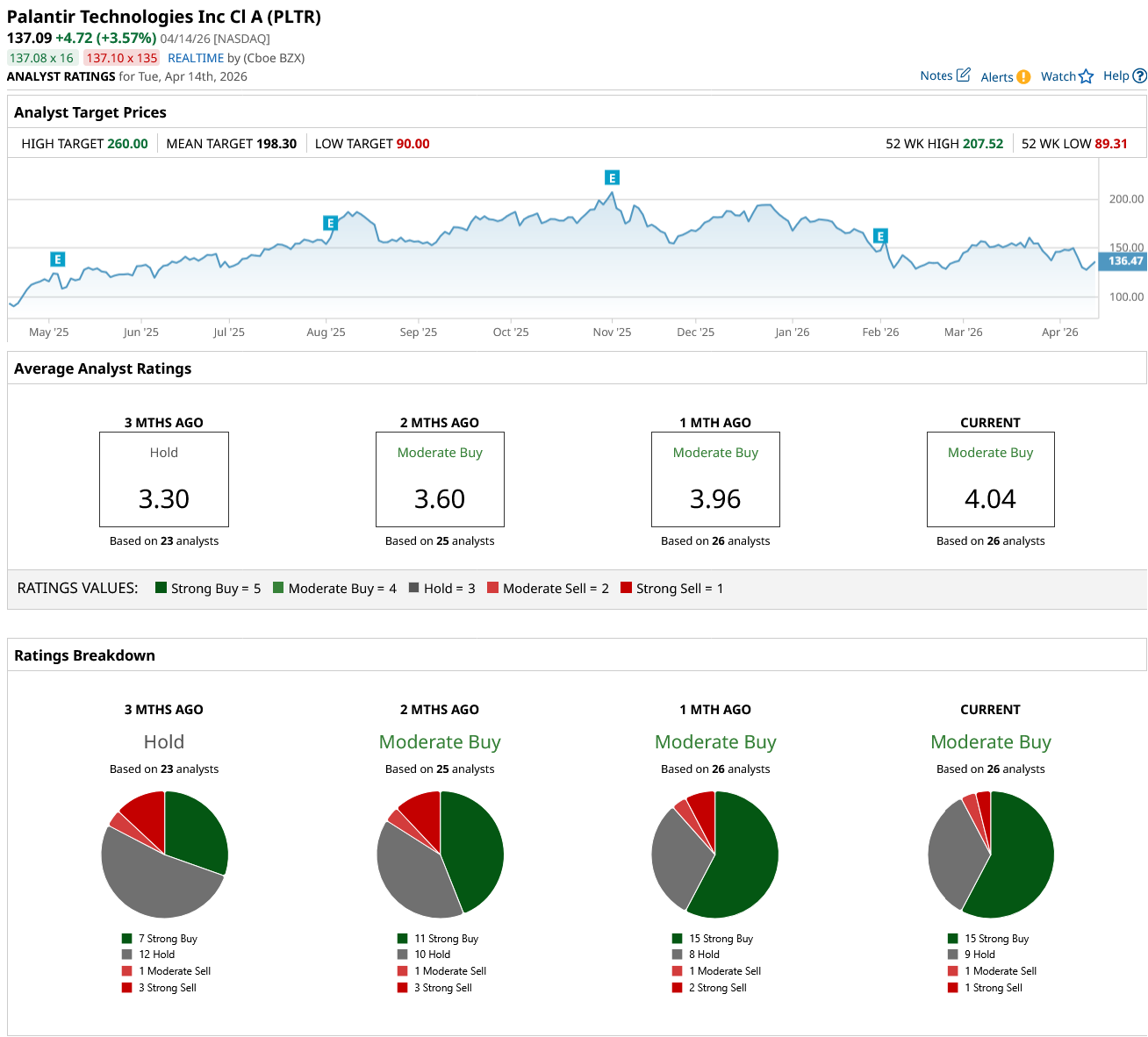

Out of the 26 analysts covering PLTR stock, 15 recommend “Strong Buy,” nine recommend “Hold,” one recommends “Moderate Sell,” and one recommends “Strong Sell.” The average PLTR stock price target is $198.30, above the current price of about $137.

Burry believes the fundamental value of Palantir is well under $50 per share. He sees the stock as wildly overvalued even at current prices and has repeatedly rolled his put options rather than closing them.

That's a bold call on a company that grew U.S. commercial revenue by 137% in a single quarter. Investors will need to weigh the bear case, a premium valuation that leaves little room for error, against an accelerating business.

On the date of publication, Aditya Raghunath did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- CoreWeave Just Scored a Major Anthropic Data Center Deal. Does That Make CRWV Stock a Buy Here?

- Is Alibaba Stock a Buy as It Reveals It's Behind the Viral Happy Horse AI Model?

- Bloom Energy Breaks Into Overbought Territory on Oracle Deal. Is It Too Late to Buy BE Stock?

- Meta Is Set to Overtake Google in Digital Ads. Is the Stock a Buy Before April 29 Earnings?