GE Vernova (GEV) stock has rallied strongly over the past year, driven by strong demand amid an evolving power and energy infrastructure landscape. Although GEV stock has maintained positive momentum in 2026 and remains up about 32% year-to-date (YTD), it has recently declined about 10% from its all-time high of $948.38. Considering the solid demand environment, expanding backlog, and improving profitability outlook, this dip presents an entry point for investors.

GE Vernova operates across several key segments of the energy value chain, supplying power generation equipment and services, grid solutions, and energy storage systems. Demand for these solutions is strengthening as investment in artificial intelligence (AI) infrastructure worldwide, primarily in data centers, continues to expand. At the same time, the electrification of transportation systems and commercial buildings is increasing overall electricity consumption, placing additional pressure on existing power infrastructure.

Beyond these structural demand drivers, the broader transition toward cleaner and more resilient energy systems is accelerating capital investment in power generation and grid modernization. This multi-year investment cycle is creating sustained growth opportunities for companies that provide critical energy technologies and services, such as GE Vernova.

Against this backdrop, GE Vernova appears well-positioned to benefit from favorable industry dynamics. With demand rising and pricing trends remaining supportive, GEV is likely to deliver strong future revenue and earnings growth, which supports its longer-term investment appeal.

GE Vernova’s Growth Outlook Remains Solid

GE Vernova’s long-term growth outlook remains solid, supported by rising demand for power infrastructure, expanding equipment orders, and improving profitability. As global electricity demand accelerates, driven by industrial growth, electrification, and the rapid expansion of data centers, GEV is well-positioned to benefit from sustained investment in power generation and grid infrastructure.

Supporting GEV’s future growth is the solid momentum in the company’s rapidly expanding backlog. During 2025, GE Vernova increased its total backlog by more than 25%, bringing it to $150 billion. This expansion reflects particularly strong order activity in the Power and Electrification segments, both of which are seeing heightened demand from utilities, industrial customers, and large technology companies.

The Power segment remains a key growth catalyst for the company. Demand for both equipment and services has strengthened as utilities invest in new generation capacity while upgrading existing infrastructure to improve efficiency and reliability. Favorable pricing conditions and increasing order activity have helped drive expansion across the segment.

Gas Power equipment demand has been strong in the U.S. This demand has led to an increase in equipment backlog and slot reservations, suggesting that order momentum could remain strong in the near term.

Equally important is the services business within Power, which provides a stable, high-margin revenue stream. By the end of the fourth quarter, the services backlog reached around $70 billion, driven largely by the Gas business. Customers are increasingly entering long-term service agreements to maintain and optimize their fleets, creating predictable recurring revenue and improving profitability visibility.

The Electrification segment is also benefiting from structural demand shifts. Investments in grid resilience, energy security, and transmission infrastructure are accelerating globally. Backlog in this segment rose to $35 billion, up $11 billion year over year, supported by traditional utilities and hyperscale data center developers, particularly in the U.S.

Meanwhile, the Wind segment is showing early signs of recovery, with fourth-quarter orders reaching $3 billion. Onshore wind activity remains steady, supported by new installations and repowering projects utilizing the company’s technology.

Looking ahead, management expects continued backlog growth in Power and Electrification through 2026, supported by strong demand and favorable pricing. Many recently secured gas turbine reservations are likely to convert into firm orders, strengthening the revenue pipeline.

The Bottom Line on GEV Stock

GE Vernova is benefiting from strong demand trends led by the rapid expansion of AI-driven data centers, global electrification, and large-scale grid modernization. With a rapidly expanding backlog, strong order momentum across Power and Electrification, and a growing high-margin services revenue position, GEV is well-positioned for long-term revenue and earnings growth.

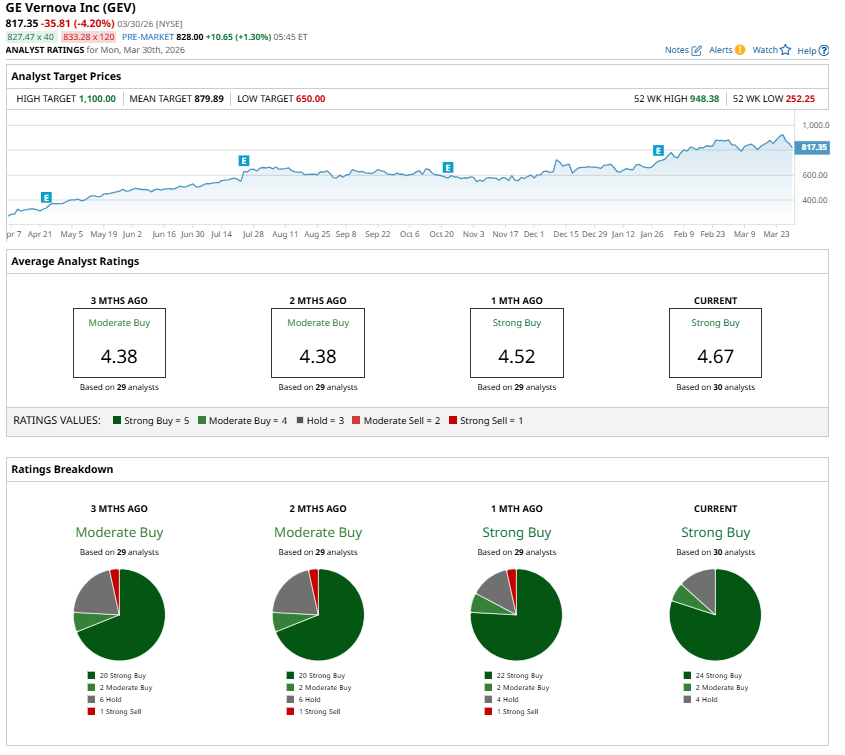

For long-term investors, the recent pullback in GEV stock presents an attractive entry point. Analysts remain optimistic about the company’s outlook and continue to maintain a “Strong Buy” consensus rating.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- GE Vernova Stock Outlook: Should You Buy the Dip in GEV or Wait?

- Huge, Unusual Put Action in Robinhood Stock - A Sign That HOOD Has Bottomed?

- Kevin O’Leary Is Rooting for a Possible ‘Game-Changer’ Move to End Iranian Control of the Strait of Hormuz: $70 Oil in Store

- While Other Markets Panic, Corn Just Got a Constructive Edge – Here's Why