The generative artificial intelligence (AI) arms race is entering a far more disruptive phase, and Anthropic’s latest advances with Claude are sending fresh shockwaves across the technology sector. What was once viewed as a productivity enhancer is increasingly being seen as a direct replacement for traditional software workflows, raising existential questions about long-standing business models.

That shift was evident this week amid a broader selloff in software stocks. The weakness followed Anthropic’s announcement that its Claude AI can now autonomously control computers, opening applications, navigating browsers, and completing spreadsheet tasks, effectively bypassing traditional software interfaces.

Moreover, reports that Amazon (AMZN) Web Services (AWS) is developing AI agents to automate sales and technical functions, work previously handled by thousands of employees, have intensified concerns that AI could compress demand for legacy software and services. These developments underscore a broader market fear that, as AI agents become more autonomous, they may erode the value proposition of many platforms.

Against this backdrop, HP (HPQ) and Intel Corporation (INTC) stand out as two of the lowest-rated IT stocks. While AI leaders are capturing the bulk of investor attention and capital, both companies remain constrained by legacy exposure: HP to a sluggish PC market and Intel to an ongoing turnaround amid intensifying competition in AI chips. And this leaves them increasingly out of sync with the destination for the next wave of value in technology creation.

Stock #1: HP

HP is an information technology company headquartered in Palo Alto, California, that specializes in personal computers, printers, and related hardware, supplies, and services for consumers and enterprises worldwide. HP currently has a market cap of $17.7 billion, reflecting its position as a mature player in the global PC and printing markets.

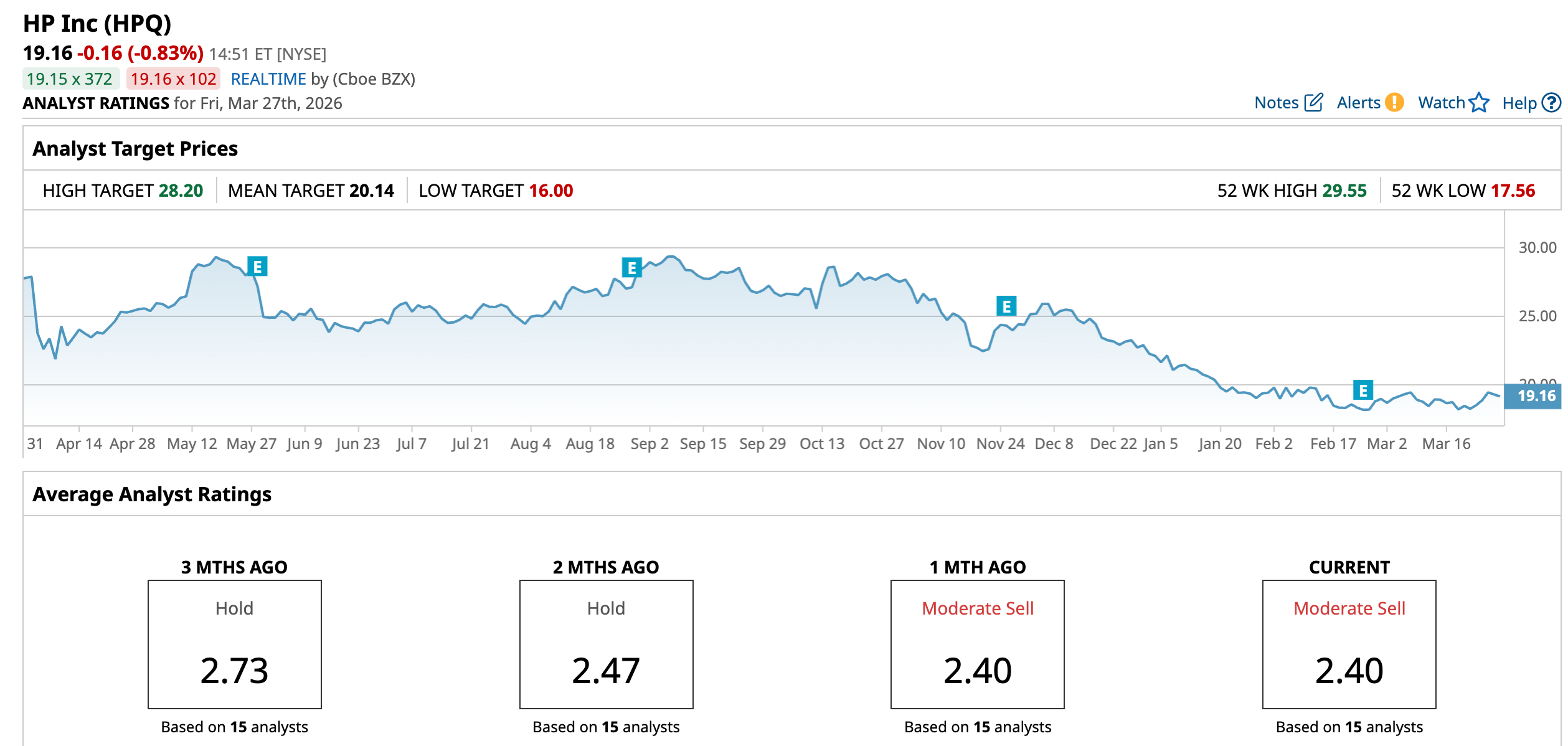

HPQ has plunged a significant 32.9% over the past 52 weeks and 13.76% year-to-date (YTD), underperforming the S&P 500 Index’s ($SPX) 12.12% returns over the past year and 6.76% decline this year.

The primary drag has been persistent weakness in the PC and printing markets, where demand remains soft and lacks strong catalysts, limiting revenue expansion. Plus, rising memory and component costs driven by AI-related demand elsewhere in the tech ecosystem have compressed margins.

Adding to the pressure, HP is seen as a relative laggard in the AI-driven shift toward high-performance computing, while its core businesses face low growth prospects and intensifying competition.

In terms of valuation, the stock trades at 6.86 times forward earnings, which is significantly lower than the sector median and its own five-year average.

HPQ reported its fiscal Q1 2026 results on Feb. 24, delivering solid top line growth alongside an improvement in adjusted profitability, though concerns around costs and guidance persisted.

The company posted revenue of $14.4 billion, up 6.9% year-over-year (YOY), driven primarily by strength in Personal Systems. Importantly, non-GAAP EPS came in at $0.81, rising 9% YOY from $0.74.

Segment performance was mixed: Personal Systems revenue increased about 11% YOY, supported by commercial demand and early AI PC momentum, while Printing revenue declined roughly 2%, underscoring structural weakness in the legacy business. Margins remained under pressure, with gross margin around 19.6%, as higher memory and component costs weighed on profitability.

Furthermore, HP guided Q2 non-GAAP EPS to $0.70 to $0.76 and maintained its full-year FY2026 non-GAAP EPS outlook of $2.90 to $3.20, but signaled results are likely to land toward the lower end of the range due to ongoing cost headwinds and a “fluid” operating environment.

Analysts tracking HPQ project the company’s profit to reach $2.84 per share in 2026, down around 9% from the prior year.

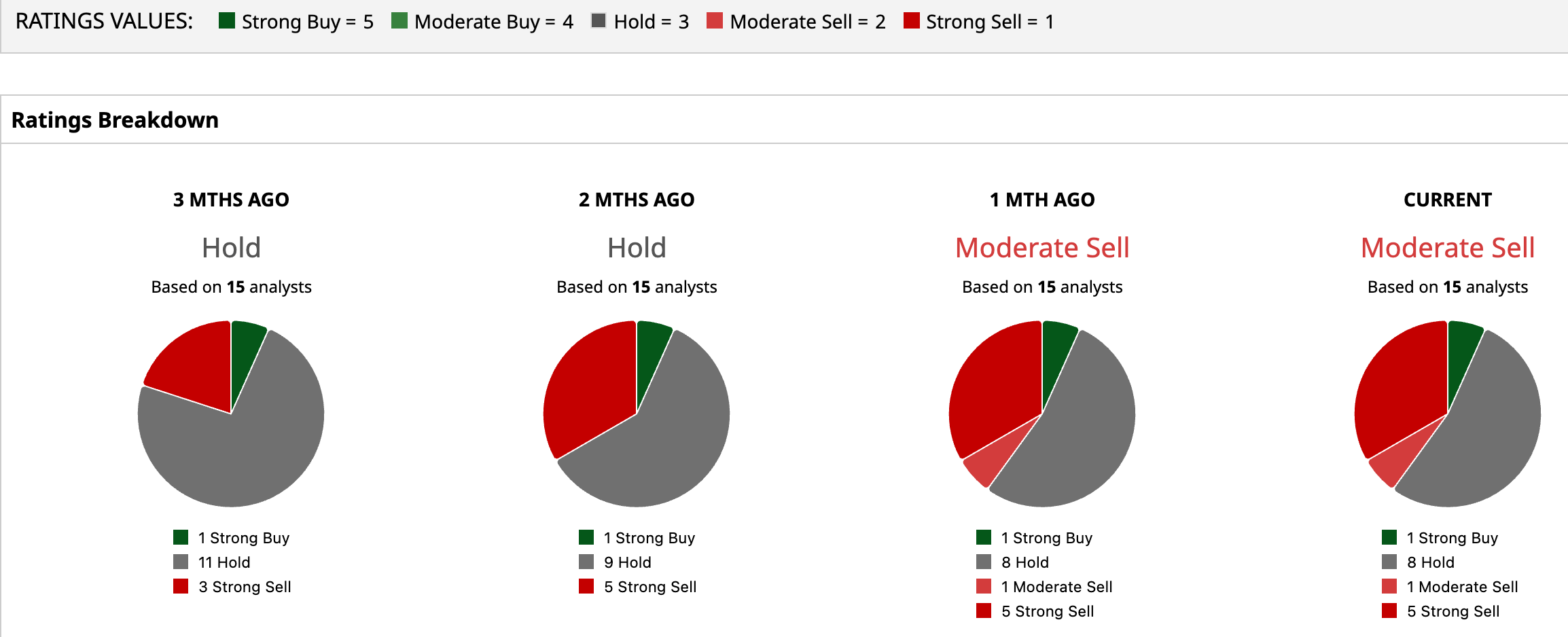

Wall Street’s outlook on the stock leans bearish, with a consensus “Moderate Sell” rating overall. Of 15 analysts covering the stock, one recommends a “Strong Buy,” eight suggest a “Hold,” one gives a “Moderate Sell,” and five advise a “Strong Sell.”

The average analyst price target of $20.14 indicates potential upside of 5.12% from the current price levels. The Street-high price target of $28.20 suggests that HPQ could rally as much as 46.7% from here.

Stock #2: Intel Corporation

Intel Corporation is a leading semiconductor company headquartered in Santa Clara, California, that designs, manufactures, and sells microprocessors, chipsets, and advanced computing technologies used in PCs, data centers, artificial intelligence, and networking applications worldwide. Intel has a market cap of $220.3 billion, underscoring its position as one of the largest global semiconductor players despite ongoing competitive and execution challenges.

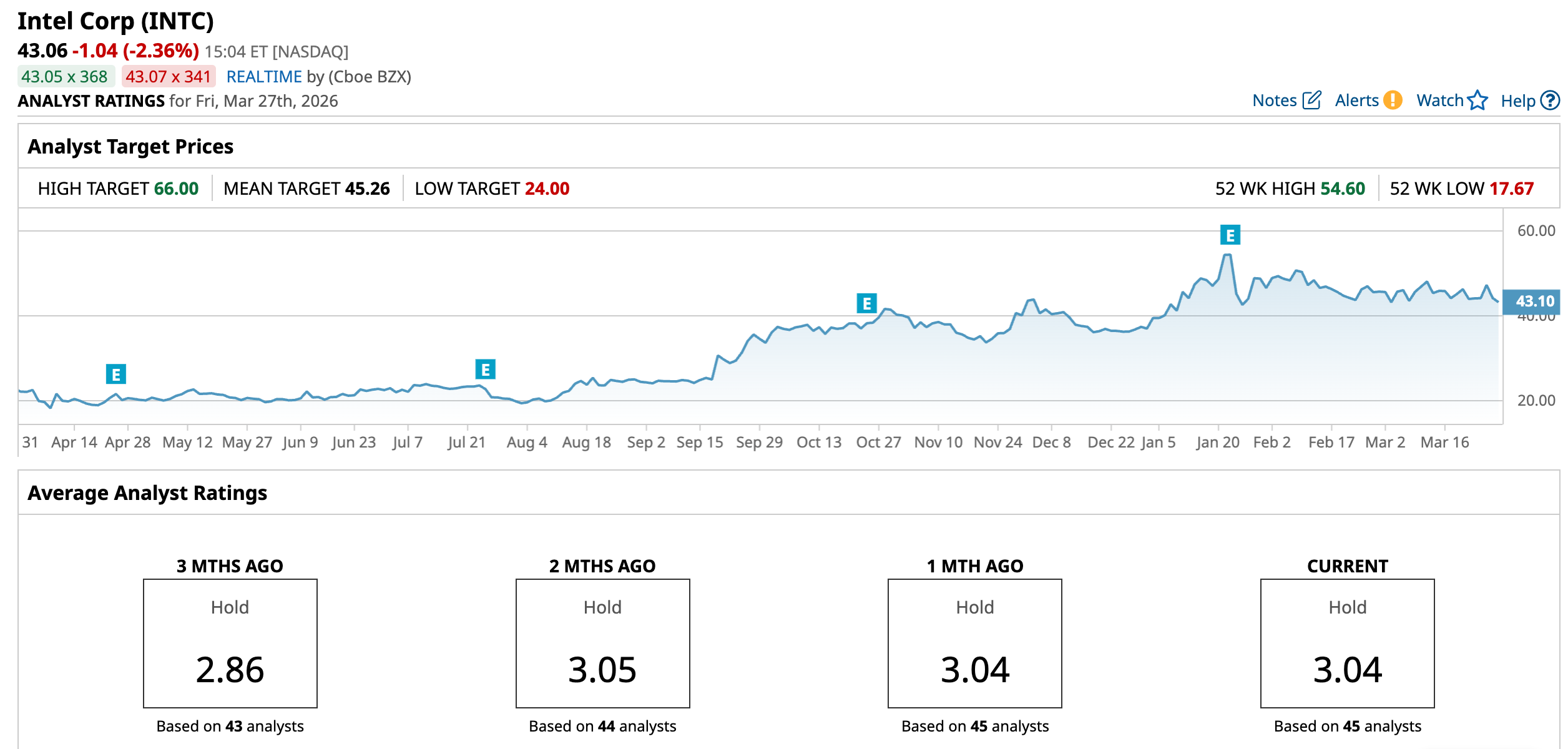

Intel shares are up 82.45% over the past 52 weeks and 16.79% YTD, outperforming the S&P 500 Index in both time frames.

Priced at 853.73 times forward earnings, the stock trades at a premium to the sector median and its own five-year average.

Intel reported its fourth-quarter 2025 results on Jan. 22, 2026, delivering an earnings beat but underscoring continued top line pressure and a cautious near-term outlook.

For the quarter, Intel posted revenue of $13.7 billion, down about 4% YOY, reflecting ongoing weakness in parts of its PC business and supply constraints. Despite the revenue decline, non-GAAP EPS came in at $0.15, up from $0.13 in the prior-year period, marking a modest YOY improvement and comfortably beating expectations. The company’s performance highlighted early progress in its turnaround, particularly with stronger demand in data center and AI-related segments, though profitability remains uneven as it remained in the red on a GAAP basis.

On a full-year basis, Intel generated revenue of $52.9 billion in 2025, essentially flat YOY compared to 2024, underscoring the company’s struggle to return to sustained growth.

Additionally, Intel issued weak Q1 2026 guidance, forecasting revenue of $11.7 billion to $12.7 billion and non-GAAP EPS around breakeven, signaling near-term pressure from supply constraints and ongoing margin compression.

Analysts tracking INTC project EPS improvement over the next two fiscal years.

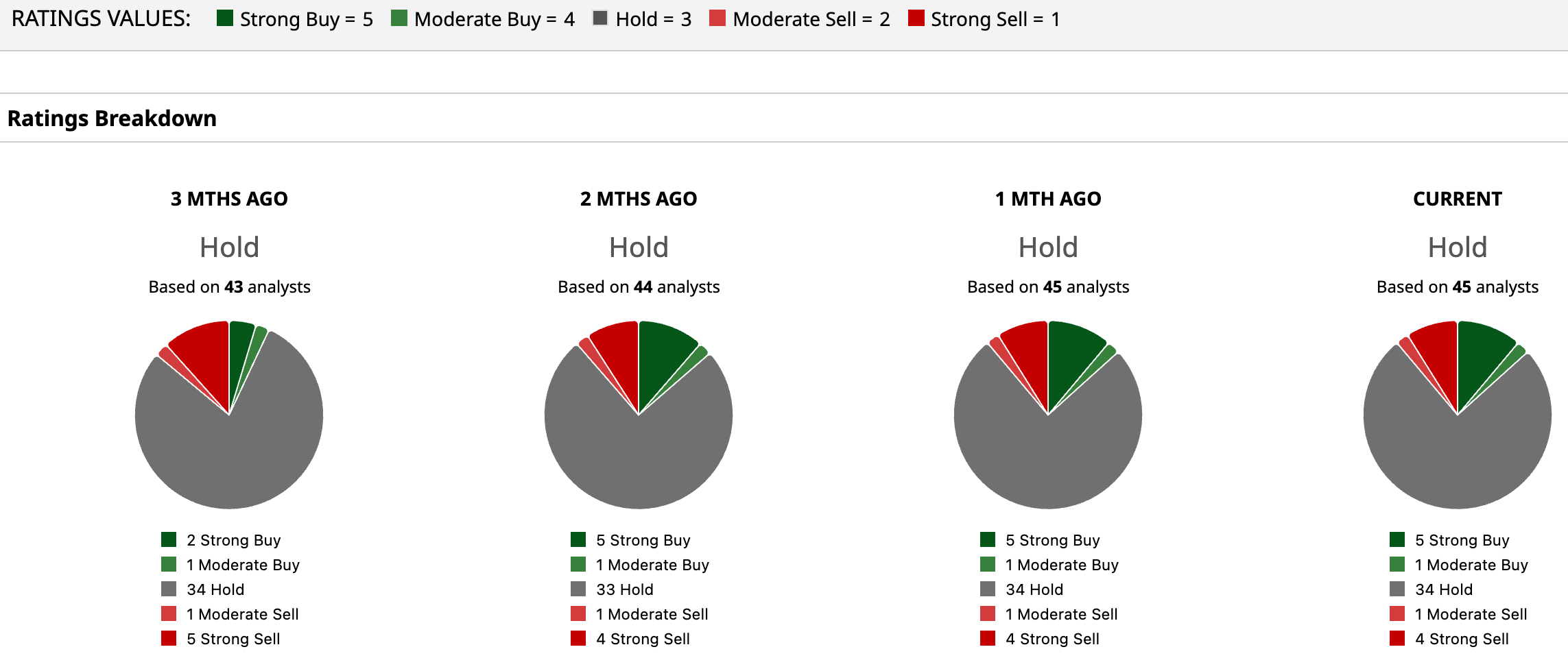

Wall Street is cautious overall, with a consensus “Hold” rating for INTC. Out of the 45 analysts covering the stock, five recommend a “Strong Buy,” one advises a “Moderate Buy,” 34 analysts are playing it safe with a “Hold,” one suggests a “Moderate Sell,” and four give a “Strong Sell.”

The average analyst price target of $45.26 indicates potential upside of 5%, while the Street-high target of $66 suggests that the stock could surge as much as 53.3%.

On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Meta Platforms Just Cut Jobs. Does That Make META Stock a Buy, Sell, or Hold Before Q2 Starts?

- As Claude Deals Yet Another Blow, Here’s Why HP and Intel Are the Lowest-Rated IT Stocks to Buy

- What Does the New Google TurboQuant Compressor Really Mean for Micron Stock?

- Only 1 of These Top 2 REITs Is Built to Pay You for Generations